House Mortgages Confusing You? Try These Tips Out

Created by-Fagan LindbergMany people don't educate themselves on how to get the best rates. Follow the tips presented here to get the best deal on a home mortgage. Keep reading to increase your knowledge.

Predatory lenders are still in the marketplace. These lenders usually prey on home buyers with less than perfect credit. They offer low or no down payments; however, the interest rates are extremely high. Additionally, these lenders often refuse to work with the homeowner should problems arise in the future.

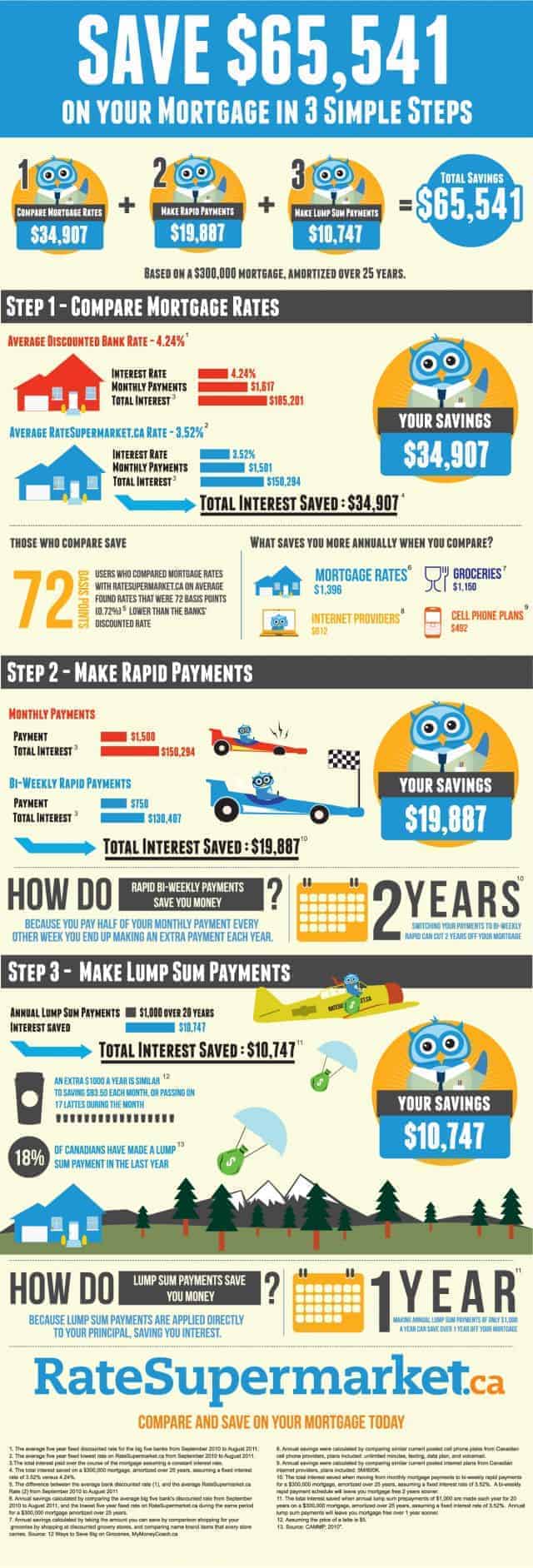

Before applying for a mortgage loan, check your credit score and credit history. Any lender you visit will do this, and by checking on your credit before applying you can see the same information they will see. You can then take the time to clean up any credit problems that might keep you from getting a loan.

Regardless of how much of a loan you're pre-approved for, know how much you can afford to spend on a home. Write out your budget. Include all your known expenses and leave a little extra for unforeseeable expenses that may pop up. Do not buy a more expensive home than you can afford.

Educate yourself on the home's history when it comes to property tax. This is important because it will effect your monthly payment amounts since most property taxes are taken from escrow. Tax assessors might value your house higher than anticipated, causing a surprise later on.

Have the necessary documents ready. There are a few documents that you'll be expected to have when you come in for a home mortgage. You'll need to provide bank statements, income tax reports, W-2 statements, and at least two pay stubs. Having these at the ready will help make your meetings go much quicker.

You are sure to need to come up with a down payment. Although there are some mortgages you can get without a down payment, for the most part you are required to have one. Find out information on the down payment requirements in advance of submitting any loan application.

Be sure to keep all payments current when you are in the process of getting a mortgage loan. If you are in the middle of the loan approval process and there is some indication that you have been delinquent with any payments, it may affect your loan status in a negative way.

Make sure you pay down any debts and avoid new ones while in the process of getting approved for a mortgage loan. Before a lender approves you for a mortgage, they evaluate your debt to income ratio. If your debt ratio is too high, the lender can offer you a lower mortgage or deny you a loan.

You can request for the seller to pay for certain closing costs. For example, a seller can pay either a percentage of the closing cost or for certain services. Many times the seller is responsible for paying for a termite inspection along with a survey and appraisal of the property.

You likely know you should compare at least three lenders in shopping around. Don't hide this fact from each lender when doing your shopping around. They know you're shopping around. Be forthright in other offers to sweeten the deals any individual lenders give you. Play them against each other to see who really wants your business.

Make sure that you have a good amount of savings before you get yourself into a home mortgage contract. There are not certainties when it comes to the economy or job stability. To protect yourself you want to have enough money saved to make your payments for many months in case the worst does occur.

During your application for a home loan, get a rate-lock. A rate-lock in writing guarantees certain terms and interest rates for a given period of time. Set the rate-lock "on application" instead of "on approval". The lock-in period needs to be long enough to allow for factors that can delay the loan process.

Make sure that you compare mortgage rates from several companies before you settle on one. Even if the difference seems to be minimal, this can add up over the years. One point higher can mean thousands of extra you will have to shell out over the course of the loan.

The best way to be sure that you take a mortgage which will continue to be easy to pay off in the future is to take less than the maximum amount you are offered. If you have some extra money at the end of the month, you can put it away into an emergency fund instead of your mortgage.

Know https://www.cnbc.com/select/best-budgeting-apps/ or home builder you are dealing with. It is common for builders and agencies to have their own in-house financiers. Ask the about their lenders. Find out their available loan terms. This could open a new avenue of financing up for your new home mortgage.

Make sure that you compare mortgage rates from several companies before you settle on one. Even if the difference seems to be minimal, this can add up over the years. One point higher can mean thousands of extra you will have to shell out over the course of the loan.

Do not give up if you do not have success getting a home mortgage. Do what you have to do to change your credit score, save some more money or whatever else you have to do to get yourself in a home. Don't, however, sign up for a mortgage that you will have trouble paying.

Be sure you are honest when you're applying for a loan. If you aren't truthful, you may be denied the loan you seek. Lenders will not have faith in you if you tell lies.

It is critical that you have an understanding of home mortgages when purchasing your first home. Ensure https://www.businesswire.com/news/home/20220308005799/en/Lili-Named-to-Fast-Company%E2%80%99s-Annual-List-of-the-World%E2%80%99s-50-Most-Innovative-Companies-for-2022 are getting the best rates by understanding the little details. Use the tips highlighted above to guarantee you're getting everything possible from your mortgage plan.